Real estate investing mistakes can turn what should be a wealth-building opportunity into a financial nightmare. While real estate has created more millionaires than most other businesses, it remains perilous territory for uninformed investors who dive in without proper preparation.

Despite its potential for financial growth and stability, many beginner investing mistakes stem from fundamental errors in judgment. You might underestimate ongoing expenses, buy emotionally rather than analytically, or skip crucial steps like home inspections and appraisals. Furthermore, beginner real estate investing mistakes often include miscalculating ROI by overestimating rental income while underestimating expenses. So why do real estate investors fail? Often because they treat investing like a hobby rather than a business, fail to conduct thorough market research, and lack clear investment goals to guide their decisions.

Avoiding these real estate investment mistakes to avoid is critical if you want to join the ranks of successful investors rather than those who learn expensive lessons. This guide walks you through 15 costly pitfalls that could derail your investment journey in 2025.

Buying Emotionally

Image Source: Sitewire

The allure of a perfect property can captivate even the most disciplined investors. Buying emotionally represents one of the most common real estate investing mistakes new investors make—one that can significantly impact your returns and investment success.

What buying emotionally means

Emotional buying occurs when investors allow feelings and subjective impressions to override logical analysis and financial considerations. Instead of focusing on numbers and return on investment (ROI), emotional buyers make decisions based on personal attachment, esthetic appeal, or intuitive reactions to properties.

According to a 2024 National Association of Realtors® report, nearly 65% of homebuyers admitted that emotional factors heavily influenced their purchasing decisions. For investors specifically, this tendency manifests when you fall in love with a property’s features, neighborhood, or potential without thoroughly analyzing its financial merits.

Emotional investors often justify their decisions with phrases like “it feels right” or “I can envision it perfectly,” rather than relying on concrete data and market analysis.

Why buying emotionally is a mistake

When emotions dictate investment decisions, several negative consequences typically follow:

- Financial overextension – Emotional buyers frequently overpay, willing to exceed market value to secure properties they’ve become attached to, straining finances long-term

- Overlooked flaws – Critical issues like structural problems, unfavorable locations, or maintenance concerns get dismissed in favor of appealing esthetics

- Impaired negotiation – Strong emotional attachment diminishes your negotiating power, potentially costing thousands in unnecessary premiums

- Neglected future value – Emotionally-driven purchases often overlook factors affecting resale value and broader market appeal

Emotional buyers may engage in bidding wars, driving prices beyond what properties are worth. Additionally, they tend to make decisions based on short-term desires rather than long-term needs, resulting in regret, stress, and potential financial loss.

How to avoid buying emotionally

To make sound investment decisions, implement these strategies to keep emotions in check:

Establish clear criteria – Before beginning your search, create strict guidelines based on investment goals. Define your non-negotiables regarding location, property condition, and financial requirements.

Take time for reflection – Never rush into decisions. Allow yourself time between viewing a property and making an offer. This cooling-off period helps clear emotional clouds that might obscure judgment.

Rely on data, not feelings – Analyze the property objectively by considering factors such as location, market trends, rental potential, and future resale value. Gather information on comparable properties to ensure you’re paying a fair price.

Involve neutral third parties – Consult with real estate agents, financial advisors, or knowledgeable colleagues who can provide objective perspectives. These individuals, not being emotionally invested, can offer candid feedback about aspects you might overlook.

Balance emotion with logic – Real estate investing inevitably involves some emotional component. The key is ensuring emotions don’t cloud your judgment of a property’s financial merits.

Remember that successful real estate investing comes from treating properties as business assets rather than emotional attachments. By maintaining objectivity, you’ll make decisions that align with your financial goals rather than fleeting emotional responses.

Waiving a Home Inspection

Image Source: LinkedIn

In competitive markets, many novice investors make the critical mistake of waiving home inspections to make their offers more appealing to sellers. This shortcut, however, often leads to significant financial consequences that could have been easily avoided.

What waiving a home inspection means

Waiving a home inspection means forgoing your right to have a professional examine the property’s condition prior to finalizing the purchase. This inspection typically includes thorough checks of the home’s systems, appliances, and structural elements. In standard real estate contracts, an “inspection contingency” gives buyers approximately 7-10 days to obtain a professional inspection report. By waiving this contingency, you surrender an important protection mechanism in the homebuying process.

Why skipping inspection is risky

The risks of bypassing a property inspection far outweigh any potential competitive advantage:

- Loss of an escape route – You sacrifice a valuable contingency that allows you to back out of the contract if serious issues arise

- Unknown safety hazards – Hidden problems like mold, pests, radon, and carbon monoxide might remain undetected

- Compromised negotiating position – Without documentation of necessary repairs, you lose leverage to request price reductions or seller credits

- Future budget uncertainty – Home inspectors can estimate the age and remaining lifespan of major components like furnaces and water heaters, helping you plan for replacements

- Insurance complications – Many insurance companies will not cover properties without proper inspection certificates

Moreover, inspection costs typically range from $300 to $600 for most single-family homes—a modest investment compared to potential repair expenses that could reach thousands or even tens of thousands of dollars.

How to ensure proper inspections

Instead of completely waiving inspections, consider these strategic alternatives:

- Conduct an “informational inspection” that gives you insights without requiring seller repairs

- Specify a financial threshold—promising not to request repairs for issues below a certain dollar amount (such as $500)

- Focus only on major structural or safety concerns, ignoring minor cosmetic issues

First-time investors often mistakenly assume that what they see during property visits tells the complete story. Nevertheless, experienced real estate professionals unanimously agree that a thorough inspection remains a crucial component of any sound investment strategy.

Waiving an Appraisal

Image Source: FasterCapital

Among the costliest real estate investing mistakes, waiving appraisals ranks particularly high for newcomers eager to close deals quickly. This decision, often made in hot markets to gain competitive advantage, can lead to significant financial setbacks and long-term consequences.

What waiving an appraisal means

Waiving an appraisal contingency means you’re forfeiting your right to have a professional assess the property’s value. Essentially, you’re committing to purchase regardless of whether the property appraises at, above, or below your offer price. In competitive situations, this makes your offer more attractive to sellers but simultaneously increases your financial exposure.

An appraisal contingency typically allows you to renegotiate or even exit the deal if a property appraises below the agreed purchase price. Once waived, you’re legally obligated to proceed with the purchase—even if you’re overpaying.

Why appraisals matter in real estate

Appraisals serve as a crucial financial safeguard for several reasons:

- Protection against overpayment – Without an appraisal, you might pay substantially more than a property’s actual worth, immediately creating negative equity

- Lender requirements – Lenders rely on appraisals to ensure they’re not lending more than a property is worth

- Future financial implications – Overpaying can complicate future refinancing, sales, and overall portfolio performance

- Market volatility buffer – Professional appraisals act as checks against market volatility, particularly important in rapidly changing conditions

Indeed, some investors discover they’ve overpaid only when attempting to sell or refinance—at which point the financial damage is already done.

How to use appraisals effectively

Rather than completely waiving appraisals, consider these strategic alternatives:

- Include gap financing in your offer, demonstrating willingness to cover a specific difference between appraised value and purchase price

- Request that sellers consider recent appraisals if they exist, possibly shortening the timeline

- Leverage strong credit and substantial down payments (20%+) to potentially qualify for automated valuation alternatives

Remember that professional appraisals provide valuable insights beyond mere valuation—they often identify condition issues and market trends that automated valuations miss.

Miscalculating ROI

Image Source: Excelsior Capital

Accurate financial analysis forms the cornerstone of successful real estate investing. Many beginner investors stumble when calculating return on investment (ROI), leading to significant financial missteps that can derail their entire investment strategy.

What ROI miscalculation looks like

ROI miscalculation typically manifests in several common forms:

- Underestimating expenses: Neglecting costs like maintenance, property taxes, insurance, management fees, and unexpected repairs leads to inflated profit projections

- Overestimating rental income: Assuming full occupancy and premium rent prices when market conditions might not support these expectations

- Ignoring vacancy periods: Every month a unit sits empty represents direct revenue loss while fixed expenses continue accumulating

- Overlooking future market conditions: Failing to analyze current trends and their potential impact on property values and rental demand

- Using estimates instead of actual numbers: Relying on rules of thumb rather than property-specific figures creates unrealistic projections

Why ROI errors hurt your investment

Miscalculating ROI creates a cascade of negative consequences. First, it establishes unrealistic expectations about an investment’s performance. Consequently, you might allocate resources to underperforming properties that drain your portfolio rather than strengthen it.

For fix-and-flip investors, ROI errors are especially damaging since profits directly connect to the time required to purchase, improve, and resell properties. Likewise, incorrect calculations can lead to overleveraging – taking on excessive debt that becomes unsustainable during market downturns or vacancy periods.

How to calculate ROI accurately

To avoid these pitfalls, implement these strategies:

- Account for all expenses: Include every cost associated with property ownership, from obvious expenses like mortgage payments to easily forgotten items like vacancy reserves

- Create conservative estimates: Project income conservatively and expenses generously to build financial buffers

- Consider financing impacts: Different loan structures dramatically affect returns; account for all financing costs including interest, points, and mortgage insurance

- Factor in appreciation realistically: Balance potential appreciation with reliable cash flow metrics rather than focusing solely on long-term value increases

By approaching ROI calculations methodically, you’ll make investment decisions based on financial reality rather than wishful thinking – a distinction that often separates successful investors from those who struggle.

Not Using a Real Estate Agent

Image Source: Lewis CPA

Many novice real estate investors attempt to handle transactions independently, believing they’ll save on commission costs—a decision that often proves more expensive in the long run.

What happens without an agent

Going solo in real estate investments comes with significant drawbacks. Without professional representation, you’ll likely face:

- Pricing errors – Statistics show that For-Sale-By-Owner properties typically sell for less than those represented by agents

- Limited market access – You miss exclusive access to Multiple Listing Services (MLS) databases and their comprehensive property information

- Legal vulnerabilities – Real estate transactions involve complex paperwork, disclosures, and regulations that require expertise to navigate properly

- Reduced negotiating power – Without a buffer between you and the seller, emotional factors may compromise your negotiating position

Studies indicate that properties sold without agents are 8-11% less likely to result in successful sales over a one-year horizon.

Why agents are valuable

Professional agents bring substantial benefits to investment transactions. Approximately 90% of residential real estate transactions involve agents, with about $100 billion in commissions paid annually. This persistence suggests tangible value, including:

- Market knowledge that helps properly value properties and identify opportunities

- Skilled negotiation that can potentially save thousands in purchase price

- Legal expertise that protects you from costly mistakes and liability

- Professional networks that connect you with inspectors, lenders, and contractors

In fact, agents often notice potential issues that investors might overlook, from structural problems to neighborhood concerns.

How to choose the right agent

For investment properties, standard agents often won’t suffice. Look for:

- Investment experience – Ideally, choose agents who are investors themselves, as they understand your priorities

- Financial literacy – Ensure they understand investment metrics like cash flow, capitalization rates, and return on investment calculations

- Local expertise – Prioritize hyper-local knowledge of neighborhoods, trends, and property values

- Proven track record – Interview multiple candidates, focusing on those handling 80-100 transactions yearly

Thereafter, consider their communication style and responsiveness, as investment opportunities often require quick action.

Failing to Do Market Research

Image Source: Investopedia

Skipping thorough market research remains one of the most detrimental errors beginner real estate investors make, potentially undermining even the most promising investment opportunity from day one.

What market research involves

Real estate market research is the systematic gathering, analysis, and interpretation of data related to property markets. This process encompasses collecting information on:

- Property values and rental rates in target areas

- Current and emerging market trends

- Consumer preferences and demographic patterns

- Economic indicators affecting real estate performance

Initially, market research might seem overwhelming, yet it’s fundamentally about building a comprehensive understanding of where you’re investing your money. At its core, this research provides actionable insights that inform investment decisions, ensuring choices are based on concrete data rather than intuition or hearsay.

Why market research is critical

Neglecting market research can severely impact your investment outcomes. Approximately 20% of new businesses fail within the first two years, primarily due to inadequate research and planning. For real estate investments specifically, the failure rates can be even more daunting.

Proper market research serves several vital functions:

- Risk mitigation – Understanding market indicators helps protect your capital investment

- Opportunity identification – Research reveals emerging trends and untapped markets

- Competitive advantage – In a field dominated by experienced players, solid research levels the playing field

- Improved ROI – Knowing where, what, and how much to invest significantly boosts returns

How to research effectively

To conduct effective market research, follow these proven steps:

- Define clear objectives – Articulate what you aim to achieve with your investment, whether focusing on rental income or property appreciation

- Analyze demographic data – Understand age distribution, income levels, and population growth patterns in your target areas

- Gather fundamental market data – Collect information on average property prices, vacancy rates, and rental yields

- Study supply and demand dynamics – Examine housing inventory, building permits, and absorption rates

- Evaluate economic indicators – Assess job growth, GDP trends, and other factors affecting market health

Finally, assemble these findings into a cohesive analysis that guides your investment decisions. Remember that successful investors aren’t just buying properties—they’re buying into markets.

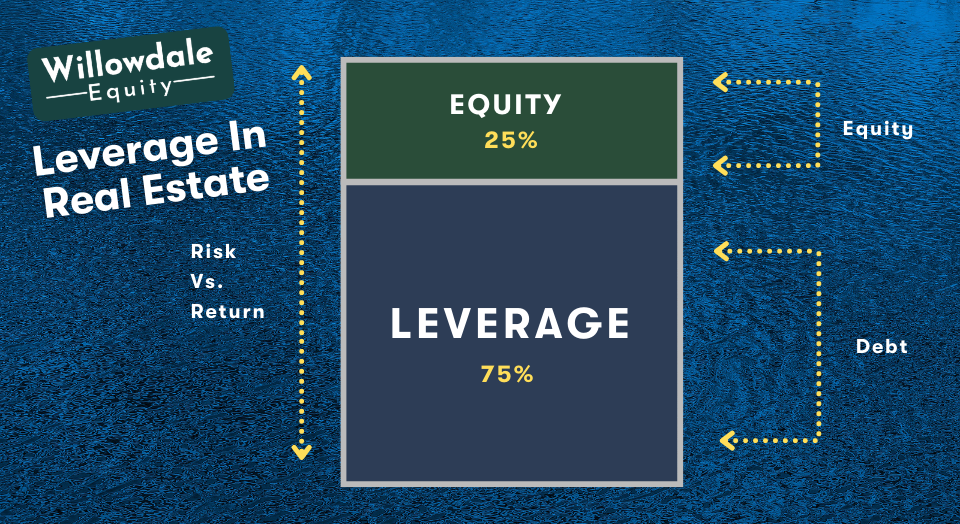

Over-Leveraging Yourself

Image Source: Willowdale Equity

Leverage stands as both the most powerful tool and the greatest threat in a real estate investor’s arsenal. When misused, it becomes a classic trap that endangers your entire investment portfolio.

What over-leveraging means

Over-leveraging occurs when investors take on excessive debt relative to property value or income potential. Although leverage allows you to control large assets with minimal capital, it becomes dangerous when your debt burden exceeds your ability to service it consistently. Typically, this happens when investors use high loan-to-value (LTV) ratios, often exceeding 80-90% of property value, leaving minimal equity buffers.

A shocking 75% of real estate investment failures occur because of excessive debt. Many investors, particularly beginners, mistakenly focus solely on potential returns while underestimating associated risks.

Why over-leveraging is dangerous

The dangers of over-leveraging become painfully evident during market downturns:

- Negative equity trap – If property values drop by just 10-20%, highly leveraged properties quickly become underwater, where loan balances exceed property values

- Cash flow vulnerability – Even minor rental income disruptions can make mortgage payments unmanageable

- Foreclosure risk – Unable to service debt, over-leveraged investors often face property loss

- Domino effect – Problems with one property can trigger defaults across your entire portfolio

Unfortunately, the 2008 financial crisis demonstrated these risks dramatically, as investors with 90% leverage faced extreme financial distress when property values collapsed.

How to manage leverage wisely

To harness leverage’s power while minimizing its dangers:

- Maintain conservative LTV ratios between 60-70%

- Ensure properties generate enough rental income to cover all debt obligations comfortably, maintaining a Debt Service Coverage Ratio above 1.25

- Conduct stress tests on your portfolio to determine how market shifts would impact your ability to service debt

- Build substantial cash reserves covering at least six months of mortgage payments across your portfolio

- Diversify financing sources rather than relying solely on traditional mortgage debt

Remember, sensible borrowing means ensuring rental income at minimum covers your mortgage payments. Balance your desire for expansion with sustainable debt levels.

Ignoring Property Management Costs

Image Source: PropertyMetrics

Hidden beneath the surface of seemingly profitable investments, property management costs represent a persistent expense that many first-time real estate investors dangerously overlook.

What property management entails

Property management involves acting as an intermediary between landlords and tenants while handling operational aspects of residential and commercial properties. These professionals typically provide tenant sourcing, rent collection, maintenance coordination, and overall property administration. Most importantly, they possess market knowledge and regulatory expertise that streamlines the rental process for both owners and tenants.

Management services aren’t free—they generally come with varied costs structured as either percentage fees (typically 8-12% of monthly rent) or flat rates. Beyond core management fees, additional charges typically include:

- Leasing fees (often equal to one month’s rent)

- Renewal fees (averaging $250 for existing tenant renewals)

- Maintenance markups (10-30% on contractor prices)

- Administrative fees for inspections and document preparation

Why ignoring these costs is a mistake

Overlooking these expenses creates a dangerous financial blind spot. First thing to remember, if you’re managing just 10 properties with hidden costs of $100 per booking, that’s $1,000 in overlooked expenses—potentially $100,000 annually with 100 bookings.

These concealed costs essentially erode your investment returns. Notably, they can transform what appeared profitable on paper into a financially draining asset. Ultimately, this oversight frequently leads to negative cash flow and prevents you from benefiting from economies of scale as your portfolio grows.

How to budget for management

To properly account for management expenses:

- Calculate all potential fees, both standard and occasional

- Include management costs in your property’s gross operating income (GOI) calculations

- Prepare multiple budget versions based on varying vacancy rates and maintenance scenarios

- Maintain reserve funds (minimum $200) for unexpected repairs

Meanwhile, consider whether self-management or professional management aligns better with your investment goals, time constraints, and expertise. For high-value investments, professional management often delivers returns that justify the costs.

Not Having an Exit Strategy

Image Source: DealRoom.net

Few real estate investing mistakes prove as destructive as neglecting to develop an exit strategy. Successful investors recognize that knowing when and how to sell a property is just as crucial as knowing when to buy.

What an exit strategy is

An exit strategy serves as your roadmap for eventually selling or liquidating an investment property. It outlines how you’ll divest from the property while realizing gains or minimizing potential losses. More than a simple selling plan, a comprehensive exit strategy includes specific timelines, financial objectives, and contingency options if market conditions shift unexpectedly.

In essence, exit strategies aren’t one-size-fits-all approaches. Each plan should reflect your unique investment goals, timeline requirements, and profit expectations. Above all, this strategy provides clarity on when to walk away, preventing emotional attachments from clouding financial decisions.

Why you need one

Failing to establish an exit strategy exposes investors to substantial risks:

- Financial uncertainty – Without clear exit parameters, you may miss optimal selling opportunities or hold properties during declining markets

- Peace of mind erosion – You’ll lack assurance that your future remains secure if unforeseen circumstances arise

- Control limitation – Unplanned exits typically happen reactively rather than strategically, reducing your negotiating leverage

- Portfolio stagnation – Being unable to liquidate investments when necessary restricts your ability to pursue better opportunities

Studies indicate that two-thirds of businesses (including real estate ventures) operate without formal exit plans, a dangerous oversight considering market volatility.

How to build a smart exit plan

To create an effective exit strategy:

- Define clear investment objectives and timeline expectations before purchasing

- Consider multiple exit scenarios (sale, refinancing, 1031 exchange) to maintain flexibility

- Analyze market cycles to identify optimal selling windows

- Establish specific financial thresholds that trigger exit decisions

- Assemble expert advisors (tax professionals, attorneys, real estate agents) to guide execution

Ultimately, smart exit planning provides control over your investments rather than letting circumstances dictate outcomes.

Focusing Solely on Appreciation

Image Source: Medium

The temptation to chase rapid wealth through property value increases leads many newcomers to make one of the most widespread real estate investing mistakes—focusing exclusively on appreciation while ignoring cash flow.

What appreciation-focused investing is

Appreciation investing centers on acquiring properties primarily for their potential to increase in value over time. This approach prioritizes future selling price over current rental income. Appreciation occurs in two forms: market appreciation (general price increases due to economic factors and demand) and forced appreciation (value added through improvements or upgrades).

Historically, real estate markets have demonstrated average annual appreciation rates between 3% and 5% over several decades. Appreciation-focused investors often target properties in emerging neighborhoods or rapidly developing areas, betting that future demand will drive substantial value increases.

Why it’s risky

Pursuing appreciation exclusively creates several significant vulnerabilities:

- Market dependency – Property values fluctuate with economic conditions, making appreciation unpredictable and sometimes negative

- Extended holding periods – Buy-and-holds for appreciation often require 10+ years to realize meaningful gains

- Cash flow gaps – Without rental income covering expenses, you must continually fund negative cash flow properties

- Timing challenges – Success depends heavily on buying and selling at optimal market points

Unlike cash-flow properties where values connect directly to rental income, appreciation-only investments face greater volatility. Throughout market downturns, these properties can quickly transform from assets to liabilities.

How to balance appreciation and cash flow

Instead of gambling exclusively on appreciation, consider a dual-focus approach:

- Target properties offering modest cash flow while positioned in growth-oriented markets

- Build a diverse portfolio including both stable high-yield rentals and emerging high-appreciation areas

- Focus on positive cash flow first, then pursue appreciation as a secondary benefit

Ultimately, successful investors recognize that appreciation represents a potential bonus, not a guaranteed outcome. Hence, establishing solid cash flow fundamentals creates resilience against market fluctuations while still allowing you to benefit from long-term value increases.

Underestimating Repair and Maintenance Costs

Image Source: Auction.com

Repair and maintenance budgeting remains a persistent stumbling block that separates successful real estate investors from those who struggle to achieve profitability. Most newcomers grossly underestimate these ongoing expenses, creating dangerous financial vulnerabilities.

What repair costs include

Repair costs encompass a surprisingly broad spectrum of expenses. These typically include:

- Routine maintenance – Regular tasks like HVAC servicing ($150-$300 annually), lawn care, pest control, and general upkeep

- Major repairs – Substantial projects such as roof replacement ($5,000-$10,000), plumbing upgrades, and structural repairs

- Emergency repairs – Unexpected issues requiring immediate attention, such as burst pipes ($250-$1,000), electrical failures ($200-$1,000), or HVAC breakdowns ($500-$3,000)

Additionally, these expenses fluctuate based on your property’s age, location, condition, and even seasonal factors. Vacant properties and those with high tenant turnover consistently generate higher maintenance demands.

Why they’re often underestimated

Underestimating repair costs occurs predominantly because investors focus excessively on acquisition while overlooking operational realities. Inexperienced investors frequently ignore long-term expenses such as appliance replacement, plumbing upgrades, and roof maintenance.

Furthermore, many beginner real estate investing mistakes stem from improper inspection during acquisition. Without thorough property evaluation, expensive underlying issues remain undetected until they require emergency intervention.

In conjunction with inadequate research, investors often lack historical data on routine maintenance needs. This incomplete picture causes them to overlook the true cost of property ownership beyond the mortgage payment.

How to plan for repairs

To avoid these real estate investment mistakes, implement structured budgeting using proven formulas:

The 1% Rule suggests allocating 1-4% of your property’s value annually for maintenance. For a $300,000 property, budget $3,000-$12,000 yearly.

Alternatively, consider the Square Footage Formula – setting aside approximately $1 per square foot annually.

Ultimately, successful investors create separate reserve funds specifically for maintenance and repairs. This dedicated account should ideally contain enough to cover at least six months of expected maintenance costs plus emergency reserves.

Preventative maintenance certainly extends the lifespan of systems and structures while reducing long-term costs. Scheduling regular inspections helps identify minor issues before they evolve into major expenses.

Failing to Diversify Your Portfolio

Image Source: Canyon View Capital

Concentrating investments in a single property type or market represents a significant vulnerability that many new real estate investors fail to recognize until it’s too late.

What diversification means

Diversification in real estate investing involves spreading investments across various assets to reduce portfolio risk. This strategic approach encompasses distributing capital across different property types (residential, commercial, industrial), geographic locations, and investment vehicles. As the Financial Industry Regulatory Authority notes, “portfolio diversification is the single-most-important strategy to deploy in an attempt to manage investment risk”. Fundamentally, diversification follows the principle of not putting “all your eggs in one basket,” creating a balanced investment approach that can withstand market fluctuations.

Why it protects your investments

A diversified real estate portfolio offers substantial protection against market volatility. When different assets react differently to market changes, your overall portfolio remains more stable during economic fluctuations. Studies show that adding broad exposure to real estate historically reduced portfolio volatility, allowing investors to achieve the same returns with lower risk levels. Subsequently, this protection becomes even more pronounced when real estate allocation is diversified by region.

Property investors with concentrated positions often experience dramatic declines in portfolio value when unforeseen developments affect their limited investments. Conversely, geographic diversification helps mitigate risks from local economic downturns, regulatory changes, or natural disasters.

How to diversify effectively

To build a properly diversified real estate portfolio:

- Diversify by property type – Invest across residential, commercial, industrial and retail properties to benefit from varying market dynamics

- Expand geographically – Target different cities, regions, or even countries to reduce location-specific risks

- Balance asset classes – Allocate portions to both low-risk, income-generating properties and higher-risk, growth-oriented investments

- Consider investment vehicles – Explore REITs, crowdfunding platforms, and direct property ownership as complementary strategies

Regularly reviewing and rebalancing your portfolio remains essential for maintaining effective diversification as markets shift.

Not Building a Team of Experts

Image Source: The Cauble Group

Going solo in real estate investing can lead directly to costly mistakes, as successful wealth-building demands specialized expertise beyond any single person’s capabilities.

What a real estate team includes

A comprehensive real estate investment team typically encompasses:

- Real estate agents/brokers who understand investment properties and local markets

- Property managers handling tenant relations, maintenance, and rent collection

- Attorneys specialized in real estate transactions and compliance

- Accountants/tax advisors with expertise in real estate investments and tax strategies

- Lenders/mortgage brokers familiar with investment property financing

- Contractors/handymen for repairs, renovations, and maintenance

- Insurance agents providing property coverage and risk management advice

- Mentors/coaches offering guidance based on their investment experience

Together with these professionals, you create a network that addresses every aspect of successful investing.

Why a team is essential

Attempting real estate investing alone significantly increases your risk of failure. As one expert notes, “real estate investing is not a business you want to go all alone”. A well-assembled team offers:

- Access to specialized knowledge across different investment aspects

- Better negotiation leverage through professional representation

- Reduced legal and financial risks through expert guidance

- Improved property management and tenant selection

- Enhanced ability to identify lucrative opportunities

Studies show that effective property management alone is critical for maximizing rental income and minimizing vacancies.

How to build your team

To assemble an effective investment team:

- Define your specific needs based on your investment strategy and goals

- Thoroughly vet potential team members by checking references, reviews, and credentials

- Build relationships based on trust, communication, and mutual respect

- Maintain clear communication to ensure alignment toward common goals

- Regularly evaluate performance of team members and make adjustments when necessary

Keep in mind that your team should evolve alongside your investment portfolio, often requiring different expertise as you grow.

Not Setting Clear Investment Goals

Image Source: Steadily

Investment success rarely happens by accident. Many new real estate investors dive into the market without defining what they actually want to accomplish—a fundamental error that undermines long-term performance and satisfaction.

What goal-setting looks like

Effective investment goal-setting establishes a clear roadmap for your real estate journey. At its core, investment goals outline specific financial targets, preferred asset classes, and investment strategies. These objectives serve as guiding principles informing your approach to real estate investing.

A well-defined investment philosophy acts like a compass, helping you make informed decisions while staying focused on long-term objectives. Your goals might include generating passive income, achieving capital appreciation, or building generational wealth through property assets.

Why goals guide success

Goals transform abstract hopes into concrete plans. They provide direction in the intricate landscape of property investment, helping you make strategic decisions aligned with your long-term vision. Without clear financial goals, you’re essentially sailing without a compass.

Goals also enable you to:

- Track measurable milestones throughout your investment journey

- Assess potential investments with confidence

- Anticipate and mitigate risks proactively

- Adapt to market changes without losing sight of your objectives

As one expert notes, “Setting specific financial targets allows you to plan your budget, allocate resources wisely, and determine suitable financing options.”

How to define your investment goals

To establish effective real estate investment goals:

- Clarify your financial objectives—determine if you’re investing for retirement, income supplementation, or legacy building

- Establish your investment timeline—differentiate between short-term goals (immediate income) and long-term objectives (capital growth)

- Apply the SMART framework—make goals Specific, Measurable, Achievable, Relevant, and Time-bound

- Align goals with your risk tolerance—understand what level of volatility you can comfortably manage

For instance, a concrete goal might be: “Within five years, invest in two properties in growth markets with a combined value of $1.5 million, achieving 5% annual appreciation.”

Treating Real Estate Like a Hobby

Image Source: Investopedia

A fundamental difference separates those who dabble in real estate and those who build wealth through it: treating investing as a business rather than a hobby. This mindset shift represents one of the most overlooked yet critical factors in determining your long-term success.

What this mindset looks like

The hobby approach to real estate investing manifests in several telling ways. According to the IRS, “a hobby is any activity that a person pursues because they enjoy it and with no intention of making a profit”. Hobby investors typically:

- Maintain incomplete or disorganized financial records

- Invest sporadically without structured systems

- Make decisions based on personal enjoyment rather than profit potential

- Lack formal business entities, dedicated accounts, or proper documentation

- Approach property management casually without strategic planning

In contrast, business-oriented investors operate systematically, documenting every transaction while maintaining separate business accounts and formal legal structures.

Why it limits success

Treating real estate like a hobby creates substantial barriers to growth. Most importantly, the IRS applies more onerous deduction rules to hobby activities, potentially eliminating tax advantages. Furthermore, regulatory changes in the industry require investors to be increasingly strategic and knowledgeable about their practices.

Without self-discipline and time management, hobby investors struggle to follow up on leads, coordinate marketing initiatives, or manage properties effectively. Accordingly, this casual approach fails to weather market volatility or build sustainable wealth.

How to treat investing like a business

To transform your approach, adopt a CEO mindset by:

- Creating detailed business systems with complete and accurate records

- Developing financial intelligence—budgeting for marketing, education, operational costs, and maintaining reserves for slower periods

- Building emotional resilience to handle rejection, failed deals, and market fluctuations

- Setting clear expectations through effective communication with clients, tenants, and team members

- Treating properties as assets requiring strategic management rather than passive holdings

Ultimately, successful real estate investing demands viewing your practice as a full-fledged business with its own responsibilities and opportunities. To discuss strategies for elevating your real estate investments from hobby to business, schedule a strategy call with Primior at https://primior.com/start/.

Conclusion

Real estate investing presents tremendous wealth-building opportunities, though success demands a strategic approach that sidesteps the pitfalls outlined in this guide. These fifteen mistakes—from emotional buying to treating real estate as a hobby—represent the common roadblocks separating profitable ventures from financial disappointments. Experienced investors understand that disciplined analysis must drive decisions rather than emotional attachments, while comprehensive due diligence through proper inspections and appraisals protects your capital investment. Indeed, accurate ROI calculations establish realistic expectations, preventing the dangerous cycle of overestimating income while underestimating expenses.

Market research remains your strongest defense against poor investment choices, revealing neighborhood trends, demographic patterns, and economic indicators that directly impact property performance. Smart investors also recognize the danger of over-leveraging, maintaining conservative loan-to-value ratios that provide cushioning during market fluctuations. Property management costs, though often overlooked, significantly impact your bottom line and deserve careful consideration in your financial projections.

Successful real estate portfolios thrive on diversification across property types, locations, and investment vehicles—creating resilience against market-specific downturns. This balanced approach pairs cash-flowing properties with appreciation potential, mitigating risk while maximizing long-term returns. Professional guidance proves equally vital, as assembling a team of specialized experts helps navigate complex transactions while identifying opportunities you might otherwise miss. You can schedule a strategy call with Primior to discuss how tailored expertise might elevate your investment approach.

Above all, treating real estate investing as a serious business rather than a casual hobby distinguishes those who build lasting wealth from those who merely dabble. Clear investment goals, detailed record-keeping, and systematic processes transform aspiring investors into successful portfolio builders. The journey toward real estate success certainly presents challenges, yet those who approach it with preparation, discipline, and strategic thinking position themselves to achieve exceptional returns while avoiding these costly mistakes.